Seventy percent of millennials (ages 21-37) believe they are not saving as much as they could.

The primary culprit?

They blame spending too much on dining out.

Many people believe the key to all their budgeting and debt woes is simply to make more money.

But, SunTrust survey found that 1 in 3 making $75,000 per year or more still live paycheck to paycheck on occasion. And, 1 in 4 respondents making over $100,000 reported living paycheck-to-paycheck as well.

Tackling a related topic, Esquire wrote two pieces 4 Men with 4 Very Different Incomes Open Up About the Lives They Can Afford and 4 Women with 4 Very Different Incomes Open Up About the Lives They Can Afford. They’re both an interesting read.

Esquire’s respondents had salary levels of near poverty, $80,000, $350,000, and $1,000,000 for the women and $1,000,000, $250,000, $53,000, and near poverty for the men.

We decided to review the experts’ advice to determine exactly how much home, car, and total you can afford based on your annual income.

How Much Debt You Can Afford Based on Your Income

Let me begin this section by clearly stating: It’s your money. We didn’t help you make it. You can spend it however you want.

But, if your living expenses and spending habits have consistently left you with more month at the end of your money, the following tips may help you break out of the paycheck-to-paycheck cycle.

Making more money can help you. However, the answer isn’t always more money if you just spend it all.

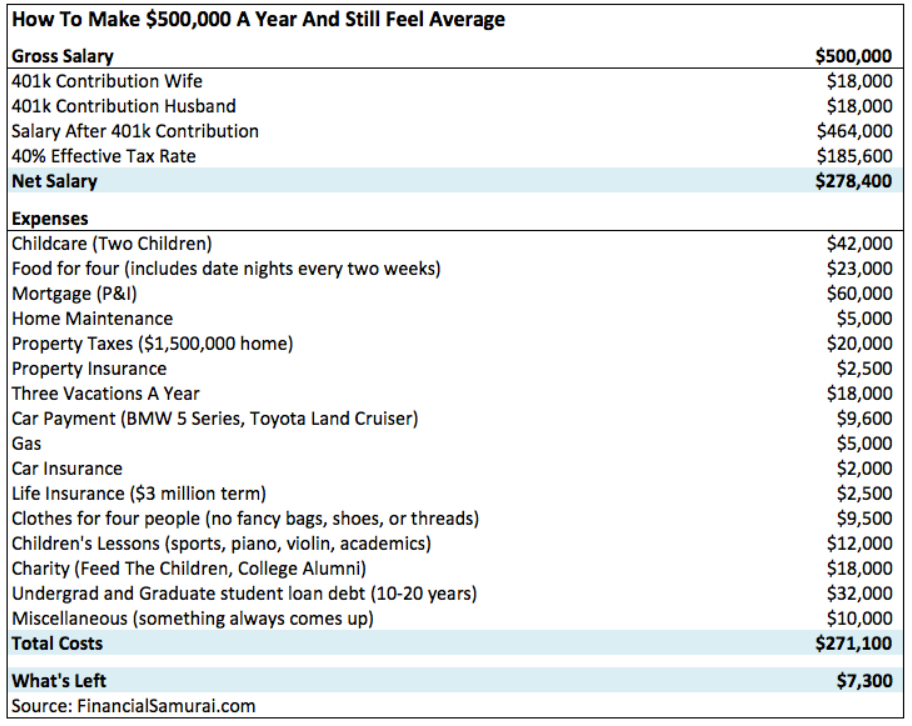

As an example, our guest and fellow blogger The Financial Samurai shared his viral piece, Scraping By On $500,000 A Year: Why It’s So Hard For High-Income Earners To Escape The Rat Race.

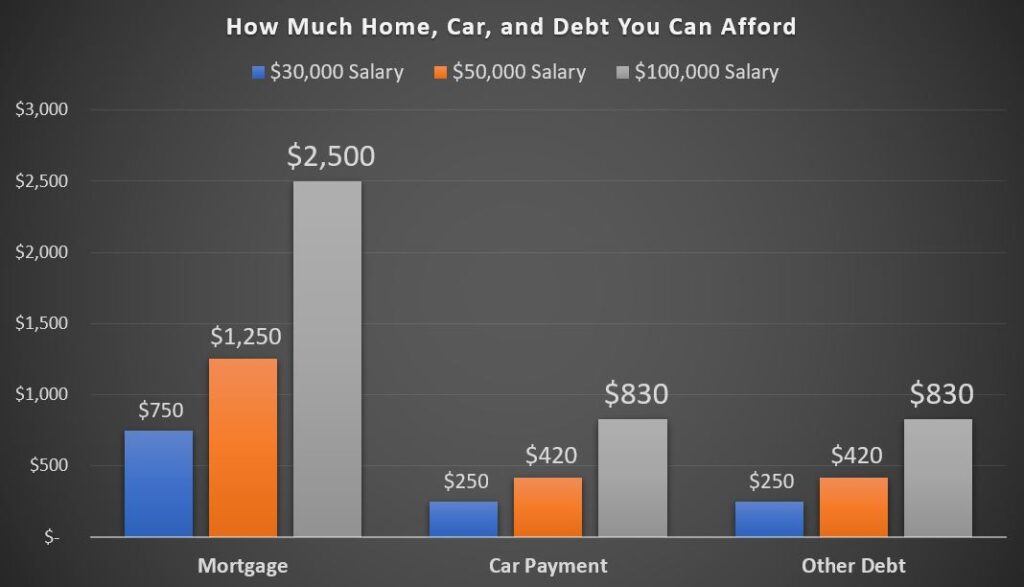

For our analysis, we’ll use three gross incomes to estimate how much home, car, and other debt you can afford if you earn an income of $30,000, $50,000, and $100,000, respectively.

To inform our conclusions, we’ll reference best practice recommendations from various industry leaders and lenders.

According to the experts, the monthly payment breakdown for each expense category is no more than:

- 30% for mortgage/housing ratio (or rent equivalent) including private mortgage insurance (PMI) and property taxes

- 10% for a car (includes principal balance, interest, and car insurance)

- 10% for debt (credit card payments, student loans, auto loans, etc.)

For our monthly income levels, that translates into the following breakdown:

So, theoretically, if your salary is $50,000 you could afford a car payment of $430 or less. With a $100,000 salary, you could afford a mortgage payment of no more than $2,500. For those with a salary near $30,000 your home, car, and debt combine should be no more than $1,250 per month.

In the real world, you are better off spending less in all three areas.

The CFPB recommends borrowers have no more than a total debt-to-income ratio (all your monthly debt payments divided by your gross monthly household incomes) of 43 percent. If your ratio is above this amount, they will recommend you not receive a Qualified Mortgage.

You can find a good rent vs buy calculator here.

For car payments, try this calculator. Remember, the rule of thumb is to spend no more than 10% of your income on your auto loan and insurance expenses.

How Much Student Loan Debt Is Too Much?

In the United States, the average student loan debt for a four-year public school undergraduate degree is over $30,000. LendEDU has a great searchable table covering over 300 majors that can help you estimate your student loan debt-to-income.

Banks are lenders.

They are not in the business of telling you how much debt you can or cannot afford. They are in the business of telling you how much debt they can lend you while minimizing their own risks that you will pay the debt back so they can maximize their profits. That’s capitalism.

It’s your responsibility to determine what lifestyle you can actually afford.

$100,000 Isn’t Always $100,000 Due to Cost of Living Differences Across the United States

Only 1 in 4 U.S. households make six figures or more. Business Insider has argued that $287,000 is the new $100,000.

How far will your salary stretch across the U.S.?

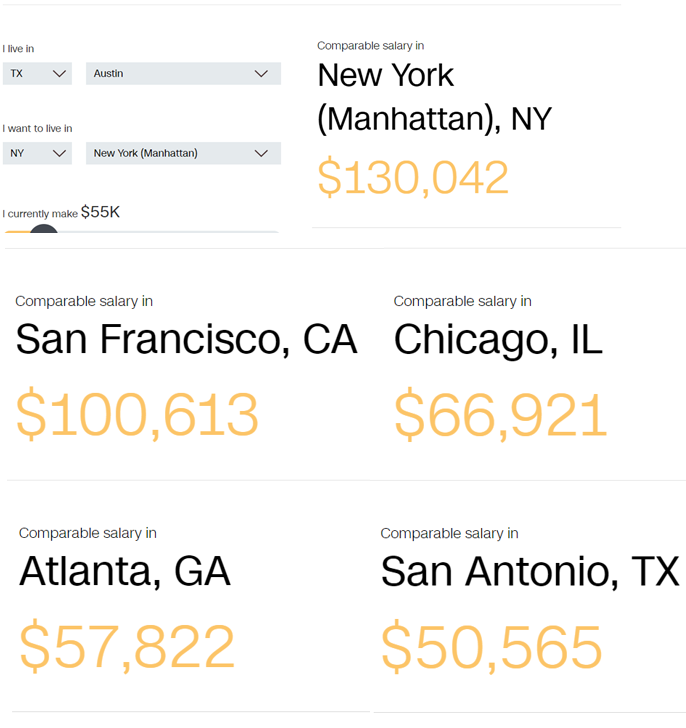

If you’re thinking of moving or relocating around the country, we recommend you use the free CNN Money Cost of Living Calculator to find out.

Let’s take CNN’s calculator for a test drive. In this hypothetical scenario, our home-based city is Austin, Texas. Based on the Cost of Living in Austin, CNN Money’s calculator estimates the comparable gross salary you will need to make to maintain your lifestyle in other cities across the country.

As you can see, the higher the cost of living the higher your salary requirements.

To maintain the same $55,000 lifestyle in Austin, Texas in a city like New York or San Francisco means you need a salary increase to reach a $100,000+ income level.

You should also observe that the cost of living can vary widely within the same state. This is why you can maintain the same lifestyle on $5,000 less if you relocate to a lower cost of living city within the same state, like San Antonio in this instance. Try the calculator for free here.

If you want an even more detailed breakdown, we recommend Bankrate’s Cost of Living Calculator. Bankrate tells you everything you need to know about cost of living changes, right down to whether your monthly budget can still afford cheese on your cheeseburgers (or avocados on your toast, for the Millennials).

Now that you know how much debt you can afford on $30,000, $50,000, or $100,000 visit our favorite Personal Finance Resources to learn how to keep even more money in your pocket and start to build wealth.

Let me go check out episode 51. I remember the $500K/year couple just scraping by. I even talked about them on my blog. I remember all of the I would never comments made. I also know that I spend money in ways a whole lot of people wouldn’t and I just shrug and say, “Oh well.”

The 500k couple. Your assumptions don’t seem right. They pay only 15% on the first 82,000 for instance. The federal rate does not go to 40 currently. You don’t take a deduction for property tax (10,000) and you assume they have no other deductions. They have an $18,000 charitable contribution that you don’t give him!

They have way too much house and the property taxes are way higher than average. They spend 1,000 per month on piano lessons and sports?

The whole thing is not realistic. Or, the people in this case are not too bright.